The continuing redistribution of Australia’s wealth, upwards

- Sep 24, 2019

- 8 min read

Updated: Nov 23, 2021

Christopher Sheil and Frank Stilwell

The recent release of the results of the ABS’s biennial survey of income and wealth met a critical response, perhaps due to a slip-shod press release. The official statistician’s headline read: ‘Inequality stable since 2013-14’. In summary, the ABS announced, ‘income and wealth inequality has remained relatively stable since 2013-14.’

The immediate difficulty was that neither the media release nor the official summary of the key findings included any statistics from the benchmark, the 2013-14 survey. To make sense of the news, commentators had to dive into the ABS’s data cubes, where they found a different story, particularly for wealth inequality, our main focus here.

Writing for the ABC, Stephen Long and Michael Janda noted the increasing divergence between the mean and median wealth trends, which is regarded by statisticians as a sign of increasing inequality. Long and Janda also found a sharp rise in the officially preferred index of inequality, the Gini coefficient, and queried how high up the ranks the ABS survey actually goes.

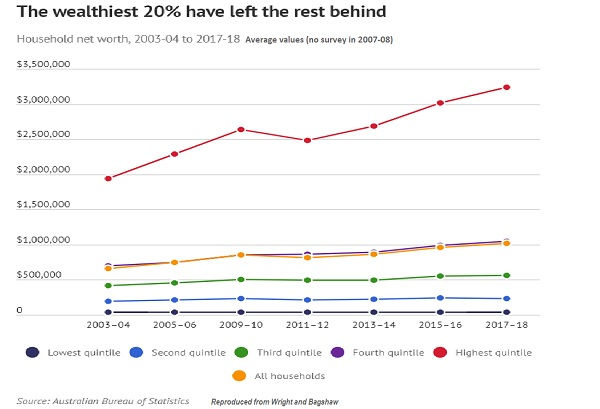

In the Sydney Morning Herald, Shane Wright and Eryk Bagshaw tracked the trends since 2003-04, when the ABS began reporting on the distribution of wealth. Looking at the data on ‘quintiles’ (which divide Australia’s households into five equally sized groups, ranging from the wealthiest 20% to the poorest 20%), they showed a deeply divided society. The captions on their charts read: ‘The wealthiest 20% have left the rest behind’ and ‘The rich are getting richer’.

Greg Jericho in the Guardian added more critical edge, and challenged the meaningfulness of the ABS’s averages. ‘On average Roger Federer and I have 4 Wimbledon titles each’, Jericho quipped on Twitter, sparking much likeminded fun (‘On average, Think Big and I have won one Melbourne Cup each’, ‘On average, the Beatles and I had 10 number one singles in the US each’).

Joking aside, the press was right not to accept the sunny headline. Drawing on the ABS’s data cubes, over the four years since 2013-14, the Top 20% of households increased their share of the nation’s private wealth from 62.1 to 63.4 per cent, up from 59 per cent in the first 2003-04 survey — while the share owned by every other quintile fell.

The second ‘wealthiest’ quintile’s share fell from 20.5 to 20.4 per cent (down from 21.3 per cent in 2003-04). The middle quintile’s share fell from 11.4 to 11.1 per cent (from 12.7 per cent in 2003-04). The second poorest quintile’s share fell from 5.1 to 4.5 per cent (from 6 per cent in 2003-04). The pathetic share of the nation’s wealth owned by the bottom 20% of households fell from 0.9 to 0.7 per cent (from 1 per cent in 2003-04).

This is not a picture of ‘stable inequality’. Rather, it is a pattern of gradually increasing wealth inequality, which is what we would expect from the underlying dynamics of modern Australian capitalism. In the absence of progressive redistribution, inequalities of accumulated wealth beget further inequalities of current income, which beget further wealth, and so on. As Thomas Piketty observed in his landmark Capital in the Twenty-First Century, the main reason why the distribution is not yet as grotesquely unequal as it was a hundred years ago, when the nobility owned practically everything, ‘is simply that not enough time has passed’.

So, let’s be clear. Unless they are actively restrained, the current trends found by the ABS suggest that Australia will continue to become an increasingly unequal society. Yet there is more to the story than getting the published data straight and none of it is cheerful.

What’s the total wealth?

First, it is passing strange that the ABS’s survey does not report a total figure for Australia’s household wealth. This means that we don’t know how much wealth the survey has missed or left out. Based on the previous survey, we will have to wait another year before the ABS publishes a total wealth figure and reconciles its findings with the household balance sheet produced as part of the national accounts.

This issue matters because the survey has always underestimated the total national wealth and the discrepancy has been growing. After adjusting for scope and measurement differences, the gap next to the national accounts was about 5 per cent in the benchmark 2013-14 survey. The gap rose to 8 per cent in 2015-16. This amounted to $626 billion, which is a lot of missing wealth. Indeed, even without a total figure, it is obvious that $626 billion is considerably more than the total wealth of the poorest 40% of Australia’s households. The largest discrepancies are conspicuously associated with an understatement of the wealth at the top of the scale, being among accounts held with financial institutions or in the form of property assets, loans, shares, trusts and other equities. In sum, while we can be sure that the proportions revealed in the ABS’s data cubes understate the inequality, we must wait to estimate the magnitude.

What’s happening with the super-rich?

The survey completely ignores the evolution of the distribution at the very top. Because the ABS reports only on quintiles, we see the share of the Top 20% but not the wealth of the Top 10% or the Top 5%, let alone the Top 1%. It is here, at the very top, where the worldwide concern over rising inequality has focused since the Global Financial Crisis, but we remain largely in the dark about the Australian situation. The only clue the ABS has given about accumulation at the top is the P90/P10 ratio, which refers to the wealth of the households at the 10th percentile measured from the bottom divided into the wealth of the 90th percentile, or the 10th percentile measured from the top.

Far from stability, the P90/P10 ratios recently published by the ABS suggest that something startling is occurring. The latest survey shows that the wealth of the 10th percentile from the top is now 71 times bigger than the wealth of the 10th percentile from the bottom. This is a record rise of almost 20 per cent on the ratio for 2015-16, which was itself a record rise of 13 per cent on the benchmark 2013-14 survey (and a rise of almost 60 per cent since 2003-04, when the ratio was a retrospectively moderate 46 times). These record-breaking jumps imply that the wealth gains of the Top 10% have been increasing much faster than for the Top 20% as a whole. It is sobering to realise, as is likely, that the soaring wealth of the 10th percentile represents around about the outer limit of the trickle-down from very much larger gains made by the Top 1%.

Among the wealthy, it seems that the most extremely wealthy are rapidly pulling further ahead. Perhaps counter-intuitively, escalating inequality is also what we would expect over a period of low economic growth. The income from labour will fall with output, disproportionately to the income from accumulated wealth. The capacity of the returns to capital to remain higher than the rate of economic growth over long periods is what Piketty dramatically described as the force by which ‘the past devours the future’.

Has the Gini any magic?

A third concern is the ABS’s over-reliance on the Gini coefficient as the primary measure of inequality. This is a time-honoured metric named after the Italian statistician who introduced it in 1914, Corrado Gini. As Long and Janda note, according to the latest survey, the Gini for wealth has risen by 2.6 percentage points to 62.1.

The Gini is a statistical artefact derived entirely from other statistics with no necessary correspondent reality of its own. This leaves room for statisticians to differ on what constitutes an economically and socially meaningful change. Statistics Canada, for example, holds that a 1 percentage point shift in the Gini matters. The ‘Godfather’ of modern inequality studies, Britain’s late Sir Anthony Atkinson, was more cautious, adopting 3 points as his standard for a significant change. The recent Australian increase rounded up is in this ballpark, except that Atkinson aimed to define a meaningful reduction, not a rise. Since 2003-04, the ABS’s Gini has increased by 5 points, well beyond Atkinson’s standard, in reverse. Again, this is not a picture of ‘stable inequality’.

More profoundly, the Gini coefficient has limitations that are coming under increasing critical scrutiny by inequality scholars around the world. As the ABS notes, the Gini coefficient is an internationally accepted summary figure for inequality, but it should be regarded as a first approximation or starting point rather than a definitive measure. By construction, it aims to measure relative inequality between 0, where every household has the same income, and 100 per cent (or 0.1, as is the ABS’s practice), where one household has all the income. Its application to wealth inequality is problematic because there is no necessary limit to how far people can fall into debt, meaning there is no necessary limit to how high a wealth Gini coefficient can rise, rendering it a conceptually distinct scale from the income Gini. This is not merely a theoretical point. The new ABS survey shows that about three-quarters of Australia’s households are in debt, and almost 30 per cent of these by three or more times their annual income.

Other issues surround the distribution’s top tail. Wealthy households have a notoriously low survey response rate. There are also problems of non-representativeness because extremely wealthy households are relatively few in number. Such errors largely account for the discrepancy with the national accounts discussed above and it is now widely recognised that they affect the Gini. One of the leading scholars associated with the World Inequality Database, Facunda Alvaredo, has developed a formula to clarify the link, adding around an Atkinson-sized 3 percentage points to the Gini in the case of the United States. The ABS has not made this adjustment. Nor has it yet followed most other OECD countries in oversampling the rich, while the top-coding (censoring) of sensitive entries has tended to undermine the usefulness of the official microdata.

Finally, there is the embarrassing fact that different distributions, including radically differently shaped distributions, can yield the same Gini coefficient. In a recent paper, Joseph Stiglitz, the American Nobel-prize winning economist, joined three Italian scholars to study this problem and they arrived at the striking conclusion that the Gini’s ability to accurately measure inequality is more the exception than the rule. Inequality has several essential properties and the Gini is only a gauge of one, concentration, which can occur in countless forms. Indeed, it turns out that the only (income) scores that can be safely relied upon are the extremes of 0 (absolute equality) and 100 (absolute inequality), neither of which exists in the real world. Between these degenerate theoretical cases, the Gini can only discriminate between distributions of similar shapes and cannot deal with overlapping shapes. One of the benefits of Italian co-authors is that we learn that Gini himself was aware of his metric’s drawbacks. Another is that the paper draws attention to the ‘Zanardi’ index, which can capture the inner differences between Gini concentrations and yield insights into the intensity and direction of inequality.

Conclusion

Statistics are windows on economic and social change and the ABS’s biennial survey gives our best view of inequality, but large areas remain fogged up. In recent research on behalf of the Evatt Foundation, we used ABS, OECD and national accounts data to estimate that, for the first time in more than half a century, the richest 10% of Australian households now own more than half the nation’s private wealth. Our methodology was commonsensical, our assumptions were conservative, and our results have held up well next to comparable sources, but our main aim is to challenge governments and others to produce better research on this critical missing link in Australia’s official inequality data. As a nation, we need better data, better analysis and better public policies if we are to address the forces making Australia a more unequal society and all that this implies, including the now well-attested harmful effects on economic growth and stability.

Christopher Sheil is a Senior Research Fellow in history at UNSW. Frank Stilwell is Emeritus Professor of political economy at the University of Sydney, and his latest book is The Political Economy of Inequality (Polity Press 2019). They are also, respectively, president and vice president of the Evatt Foundation.

Suggested citation

Sheil, Christopher and Stilwell, Frank, 'The continuing redistribution of Australia’s wealth, upwards', Evatt Journal, Vol.18, No.2, September 2019.<https://evatt.org.au/papers/continuing-redistribution-australias-wealth-upwards.html>

Comments